🔍 Key Trends in Chicago Area Residential Real Estate (Q1 2025)

As the first quarter of 2025 wraps up, Chicago's residential real estate market is showing signs of both resilience and recalibration. While closed sales lag behind last year’s numbers, buyer activity is picking up—evidenced by a strong surge in properties going under contract. Inventory remains tight, and prices continue to climb, pointing to a market that still favors well-positioned sellers. Understanding the latest market dynamics is key to making informed decisions, whether you're thinking of buying, selling, or investing. Here's a breakdown of where things stand heading into spring.

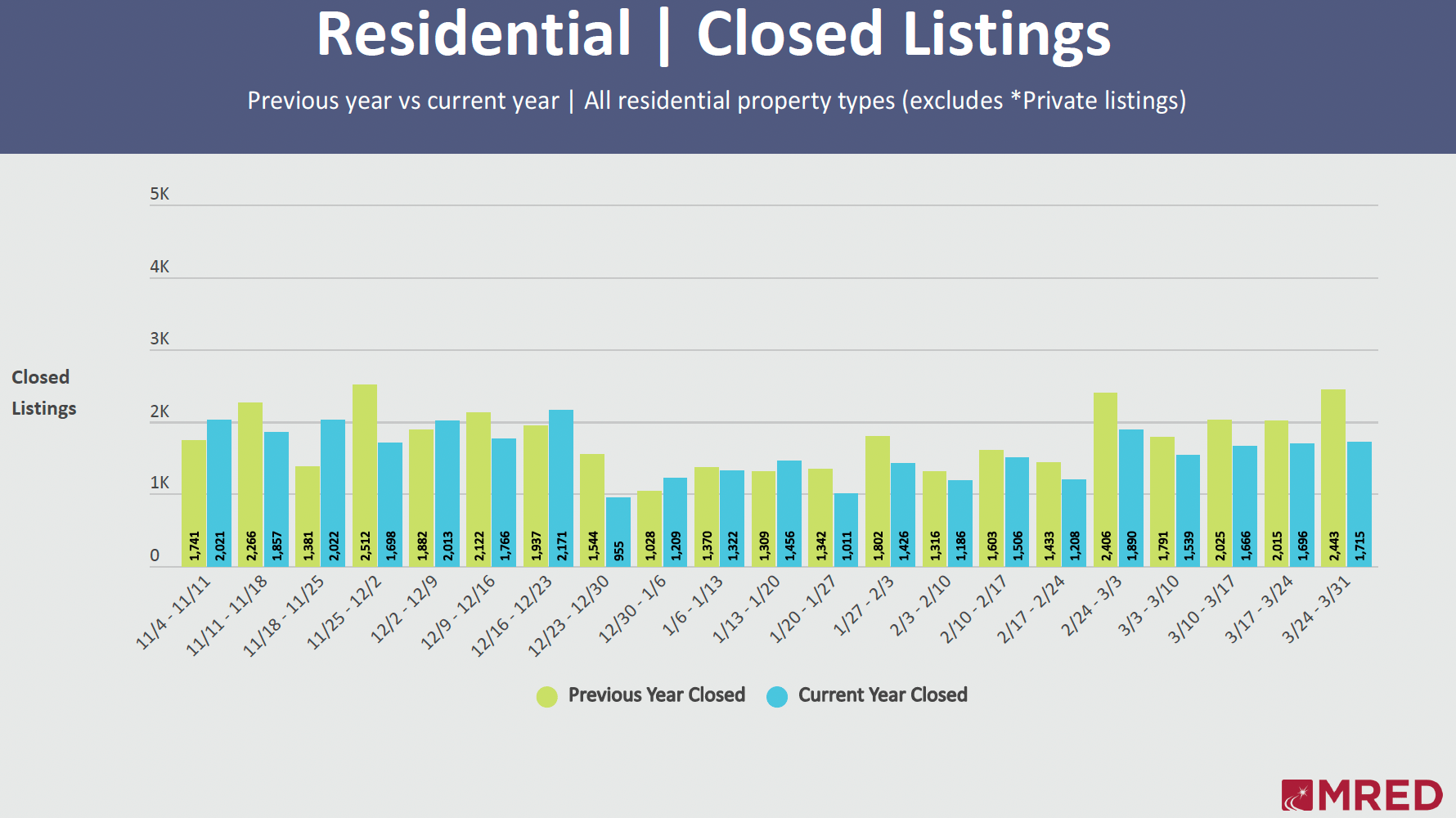

📉 Closed Sales

-

Sales volume is down compared to Q1 2024. Weekly closed listings often trailed the prior year by 200–500 transactions.

-

Slower closings suggest a combination of buyer hesitation, rate sensitivity, or inventory issues.

📝 Under Contract Activity

-

Under contract volume outperformed 2024 most weeks starting mid-January.

-

Strongest surge: early March, where 2025 saw 5,067 contracts vs ~3,000 in 2024 — up ~70% YoY.

-

Indicates pent-up demand is still present, and buyers are moving despite broader headwinds.

🏘️ New Listings

-

Listings are consistently trailing 2024, especially from January through mid-March.

-

Weeks like 2/3–2/10 showed ~40% fewer listings than the same week last year.

-

Supply tightness continues, which could sustain pricing despite slower demand.

💰 Sold Prices

-

Median sale prices increased steadily over the quarter:

-

Started near $290K, ended around $330K.

-

Average prices also climbed, reflecting strength in higher-end segments.

-

-

While volume lags, pricing remains resilient or rising, signaling seller leverage in move-in ready, well-priced inventory.

🔄 Active Inventory

-

Inventory rebounded in March to ~2,500–2,700 units weekly (after dipping below 2,000 early in Q1).

-

Still tight by historical standards, limiting buyer choices and keeping prices elevated.

🔑 Rentals

-

Consistent rental activity with ~1,500 units rented per week.

-

Median rent prices rose from ~$2,000 to $2,250+ through Q1 — mirroring purchase price trends.

-

Indicates continued strong rental demand, especially with purchase affordability challenges.

🏡 Open Houses

-

Gradual build-up in open house activity with increased momentum in March.

-

Suggests growing buyer interest and preparation for spring market ramp-up.

📈 What This Means for Strategy

-

Sellers: Pricing power remains strong for well-prepared properties. Leverage current tight inventory but act before spring inventory builds.

-

Buyers: Be ready to move quickly—under contract activity is heating up. Fewer listings mean more competition.

-

Investors/Landlords: Rising rental prices and consistent absorption make this a solid quarter for holding or adding rentals.

Conclusion

Chicago’s Q1 2025 real estate market reveals a shifting landscape: fewer new listings, steady buyer demand, and rising prices. While closed sales are down year-over-year, a spike in under-contract activity suggests momentum is building as we head into the spring market. For sellers, limited competition and strong pricing trends offer an opportunity to stand out. For buyers, acting early—before inventory and competition increase—could be the key to securing the right home. Whether you're looking to buy, sell, or invest, staying informed and strategic will be essential in navigating what’s ahead.